Role of Gas and Existing Gas Infrastructure in Climate Neutral Europe

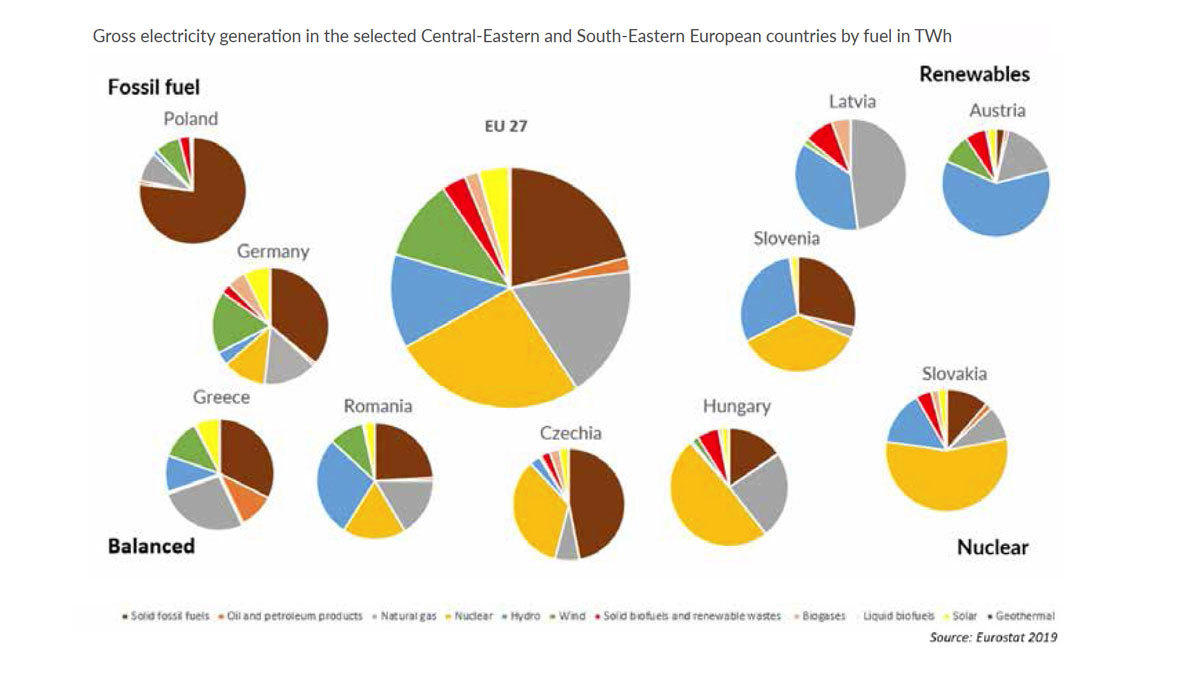

GIE publishes an in-depth analysis of the role of gases and the existing gas infrastructure in supporting Central-Eastern- and South-Eastern- Europe towards climate neutrality by 2050. The research covers 10 EU Member States, including Austria, the Czech Republic, Germany, Greece, Hungary, Latvia, Poland, Romania, Slovakia, and Slovenia.

“This analysis shows that one thing is clear: there is no one size fits all solution. If we want to deliver climate neutrality by 2050, the specificities of all EU Member States must be considered when designing Europe’s decarbonisation pathways. It will be a mistake if future legislation will ignore this. Only an inclusive and technology-neutral approach will help Europe deliver its 2050 goal. Each Member State will face its own battles and leverage its unique opportunities, but no one should be left behind,” Boyana Achovski, Secretary General of GIE, states.

“For example, due to their transit character and historical circumstances, countries in South-Eastern and Central-Eastern Europe have their energy mix strongly based on coal. Therefore, the existing gas infrastructure will play an important role when switching from coal to natural gas to hydrogen. Building on our well-developed infrastructure, the gas assets will gradually accommodate growing shares of renewable and low-carbon molecules, including hydrogen. Today, it already provides increased flexibility in complementing the electricity systems by storing a huge amount of renewable and low-carbon molecules. On top of that, our pipelines, underground storage facilities and LNG terminals can be fit for hydrogen with some retrofitting and repurposing,” she explains.

Achieving decarbonisation by 2050 requires significant efforts and commitment from all Member States and sectors. The report Decarbonisation in Central-Eastern and South-Eastern Europe: How gas infrastructure can contribute to meet EU’s long-term decarbonisation objectives brings forward the decarbonisation potential of the gas infrastructure in that context. It presents multiple pathways in which a future-proof gas infrastructure could ensure resilient security of supply by integrating large volumes of renewable and low-carbon molecules, including natural gas, hydrogen, and biogases.

Report highlights

- By 2030: Switching from coal to gas is expected to be an intermediate step in transitioning to a zero-carbon economy. Coal-based total CO2 production in the ten selected countries equalled 645,9 Mt CO2 in 2018, which is equivalent to the overall emissions generated in France and Spain (656 Mt CO2).

- By 2050: Renewable and low-carbon gases will complement and slowly replace natural gas. These gases will play a major role in the future energy system as they will secure a baseload energy supply in these regions. Renewable gases like green hydrogen will gradually adopt the role of integrating the electricity and gas sectors, providing more flexibility within the entire energy system.

- The existing gas infrastructure supports the integration of renewable electricity in Europe and reduces the need for large investments into electricity grids – on both transmission and distribution levels.

- In the short-term, natural gas can have an immediate and tangible positive effect on the life of EU citizens: air pollution resulting from burning high-emission fuels (including NOx, SOx and fine particles) constitutes a serious health problem in many communities.

- Each country is moving towards decarbonisation in a different way. The common denominator is the shared awareness of the issues at stake, their urgency as well as a strong push for efficiency.

“The main goal of this report is to raise awareness about the current energy landscape and challenges in Central- and South-Eastern European countries and to showcase these aspects with concrete and actual data. In January 2020, we established a working group to exchange views on the decarbonisation in these respective regions and this platform enables us to provide input to various stakeholders – academia, policy makers, industry representatives. The discussions and the work so far enabled us to identify the optimal energy transition pathways for the regions,” Piotr Kuś, Sponsor of GIE CH4 Area and GIE board member explains.

“The gas infrastructure plays an essential role in decarbonising the regions, both in the short- and long-term. It provides for the switch from coal to natural gas to hydrogen and it plays a role as an enabler of the energy transition towards low-carbon gases. It brings further benefits via fostering security of supply and establishing a competitive EU energy system. Using the existing gas infrastructure offers a cost-effective solution for customers, which is crucial when fostering social acceptance and cost efficiency towards the energy transition. The coal-based power and heat plants generation causes a high level of pollution on top of CO2 and causes decrease of air quality standards. In that case, natural gas will play an important role as a solution for challenging fast and cost-effective mitigation of air pollution which is caused by a mixture of solid particles and various gases. Their reduction is of crucial importance as some air pollutants like particulate matter and NOx and SOx are poisonous for the people,” he added.

Romania committed to contribute to the achievement of the decarbonisation target of the EU

Romania’s energy mix is quite balanced with a high share of solid fossil fuels, hydro, natural gas, and nuclear power. Romania has significant resources of natural gas which, can contribute to the security of supply of the country.

The natural gas market features a rather high level of concentration with the two main large producers, i.e., OMV Petrom and SNGN Romgaz, holding together a market share of over 90 % of the natural gas production. As for the market shares of main suppliers, there is a slight differentiation between the free market and the regulated market, the latter featuring a higher level of concentration.

Having a look at the projected trend in the natural gas-fired capacity, we see that the Development and Decarbonisation Plan for CE Oltenia 2020-2030 provides for an additional natural gas-fired capacity of 1400 MW as from 2024. Considering the age of the current natural gas-fired units, it has been estimated that the decrease due to their decommissioning will exceed the increase resulting from the new capacity.

Nevertheless, the gross energy production from natural gas will increase (due to increased efficiency of new capacity and increased utilisation rate of existing ones).

The level of ambition regarding the share of renewable energy was revised compared to the initially proposed share of 27.9% to 30.7%. The new target was mainly calculated based on the Commission’s recommendation to align the national macroeconomic projections to those in the ‘Ageing Report: Economic and budgetary projections for the EU-27 Member States (2016-2070)’, correlatively decommissioning the coal-based units.

In order to reach the ambition level regarding the share of renewable energy of 30.7% in 2030, Romania will thus develop additional RES capacity of approximately 6.9 GW compared to 2015. To achieve this target, appropriate funding from the EU is needed to invest in the adequacy of electricity grids and flexibility in the production of RES-E. This goal will be achieved by deploying backup gas capacity and storage capacity, and by using smart electricity grid management techniques.

Romania has chosen to adopt a prudent approach to the level of ambition, taking into account the national particularities and the RES investment demand for both replacement of units that have reached the maximum operation period and new ones in order to achieve the targets of the NECP. The replacement of existing conventional power generation capacity with low carbon capacity will also result in the further promotion of renewable resources in the production of energy (e.g., wind or solar energy), including for heating in SACET type district heating systems, energy transit through the National Energy System (NES), and the use of heat pumps at source level, as well as using the energy market mechanisms.

The replacement of the existing power and heat generation capacity will also result in the reduction of own consumption for process purposes, in particular as a result of investments in the refurbishment and development of high-efficiency cogeneration units (including methane gas-fired ones).

Projections for 2030 show an increase of up to 5,255 MW in the wind capacity and of approximately 5,054 MW in the photovoltaic capacity.

Romania plans to make a fair contribution to the achievement of the decarbonisation target of the EU and will follow the best environmental protection practices. The application of the EU ETS scheme and compliance with the annual emissions targets for the non-ETS sectors are the main commitments to achieve the goal. For the sectors covered by the EU-ETS scheme, the overall emissions reduction target of Romania reaches approximately 44% by 2030 compared to 2005.