Europe at the Top of Hydrogen Electrolyser Projects

According to Aurora Energy Research, the vast majority of electrolyser projects are located in Europe (85%), with Germany the clear front-runner with 23% of planned electrolyser capacity globally.

Germany remains the most attractive market for low carbon hydrogen investment in Europe, despite promising policies and strategies recently being released by Italy, Poland, and the UK.

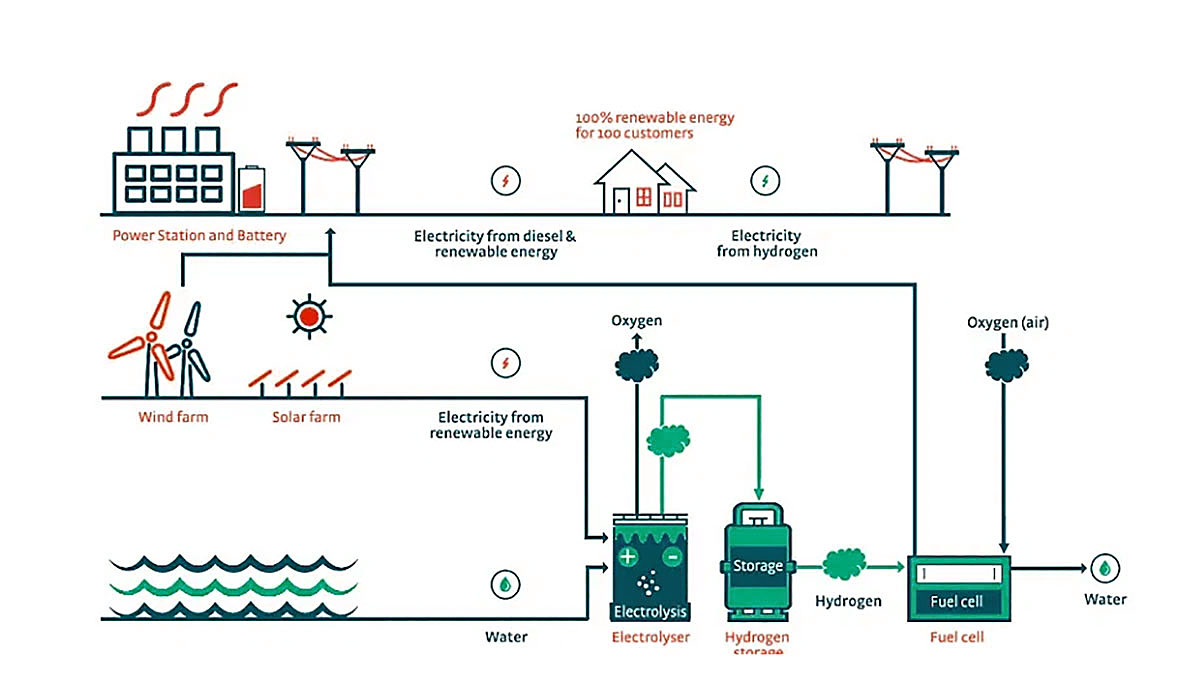

Key success factors for ‘green’ hydrogen from electrolysers are the cost and carbon footprint of electricity. France currently offers the lowest wholesale power prices, and its grid carbon intensity is one of the lowest in Europe. However, hydrogen made directly from renewable energy rather than the power grid can achieve the lowest carbon footprint. This may be the only type of hydrogen that can meet the carbon intensity thresholds set by the EU.

The UK and Europe have set challenging targets for Net Zero emissions by 2050, involving switching energy consumption across the whole economy to zero-carbon sources. Hydrogen could play an important role in reducing emissions particularly in ‘hard to abate’ activities in industry, heating, and heavy-duty transport.

Since defining Net Zero targets, governments around Europe have turned significant attention to the potential of low carbon hydrogen, which can be produced either from electrolysis of water (‘green hydrogen’) or from natural gas with CO2 capture (‘blue hydrogen’). Many governments in Europe are especially promoting electrolysers; the EU targets 40 GW of electrolyser capacity by 2030, and national governments in Europe combined have already pledged a total of 34 GW by the same date.

Green Hydrogen: global development pipeline and projects size is scaling up rapidly

The new report by Aurora Energy Research, highlights just how quickly companies are responding to this opportunity and developing new hydrogen production facilities. Drawing on its global electrolyser database, Aurora finds that companies are planning electrolyser projects totalling 213.5 GW for delivery by 2040 – of which 85% of projects are in Europe. Excluding the early-stage projects, which are in a conceptual planning phase, within Europe, there is a pipeline of over 9 GW in Germany, 6 GW in the Netherlands, and 4 GW in the UK, all scheduled to be operational by 2030. Current global electrolyser capacity is just 0.2 GW, mainly in Europe, meaning that if planned projects deliver by 2040, capacity will grow by a factor of 1,000.

Electrolyser project sizes are scaling up very quickly too as the technology and supply chain matures: to date most projects have been between 1-10 MWs. By 2025 a typical project will be 100-500 MWs, typically supplying ‘local clusters’, meaning that the hydrogen will be consumed locally to the facility. By 2030, typical projects are expected to scale up further to 1 GW+, with the emergence of large-scale hydrogen export projects, deployed in countries benefiting from cheap electricity.

Electrolyser project developers are exploring a range of different business models in terms of the power sources they harness, and the end user of the hydrogen produced. Of the projects that state a power source, most will be using wind power, followed by solar, with a smaller number of projects utilising grid electricity. A large portion of the electrolysers indicate that the end user will be industry, followed by mobility.

Hydrogen Market Attractiveness Rankings: Germany retains its leading position

Aurora’s biannual Hydrogen Market Attractiveness Report assesses the most attractive countries in Europe to invest in for low carbon hydrogen, based on policy, incentive schemes, production costs and likely centres of hydrogen demand. Although Germany still offers the most attractive market for low carbon hydrogen development, in the last six months both Poland and Italy have released their hydrogen policies. Italy’s is a long term, strategic policy – positioning itself as a hydrogen bridge between Africa and Western Europe – and aiming to convert 20% of final energy consumption to hydrogen-derived sources by 2050. Poland has released a policy focusing on shorter term goals, including a 2 GW electrolyser build target and a plan to introduce its own Carbon Contract for Difference scheme by 2025, which will encourage more expensive, low carbon production methods.

The success of green hydrogen from electrolysis will be driven by two key factors: the cost of the power – which makes up most of the cost; and the carbon footprint. For grid-connected electrolysers, France is expected to have the lowest grid power prices to 2040, followed by Germany. The countries with the lowest grid carbon intensity will be Norway, Sweden, and France. To achieve the lowest carbon footprint, electrolysers can bypass the grid and connect directly with renewable power sources such as wind, solar and hydro. The European Union is starting to determine carbon footprint thresholds within their laws and policies which will increasingly reserve the label of ‘sustainable’ hydrogen to renewable-connected electrolysers only.

On 21st April 2021, the European Commission approved a Draft Delegated Act containing a new classification for ‘sustainable’ hydrogen. The Draft Delegated Act of EU Sustainable Finance Taxonomy requires a reduction in lifecycle emissions of 73.4% relative to a fossil fuel comparator of 94 gCO2e/MJ, implying a limit of 3 tCO2/tH2. For hydrogen production using grid electricity, this equates to a grid carbon intensity of 53.3 kgCO2e/MWh, before considering other sources of emissions. This is a relatively low threshold, which Aurora expects only the power grids in Norway, Sweden, and France could meet by 2030.

Aurora revises its analysis and ranking of Hydrogen prospects in European countries every six months. Analysis on electrolysers is based on Aurora’s global electrolyser database which tracks all existing and planned electrolyser projects.

“Companies are already betting on the hydrogen economy by investing in projects now. The pipeline of electrolysers is over 200 GW, which is one thousand times the current installed capacity. If all of this capacity were to come online, it could produce up to 32 million tonnes of hydrogen per year, already half of today’s hydrogen demand,” Anise Ganbold, Global Energy Markets Lead at Aurora Energy Research, commented.

“The growth of the hydrogen electrolyser pipeline, to more than 200 GW globally, is an early indication of the rapid rollout of hydrogen infrastructure that we are likely to see in the coming years. However, there remains a significant gap in costs between ‘green’ hydrogen production from electrolysers, and existing, carbon intensive hydrogen sources. Governments across Europe have set out ambitious plans for hydrogen to drive the decarbonisation of industry and other parts of the economy, but electrolyser projects are still held back by red tape combined with a lack of specific policies and incentives,” Richard Howard, Research Director at Aurora Energy Research, added.