Pros and cons: Revival time for oil and gas industry

The chances for oil prices to return to the ascending trend to levels above USD 50-60 per barrel are increasingly higher, both oil and gas industry experts and specialized analysts say. The growth trend in global oil demand, overlapped on a process of an increasing depletion rate of the deposits under exploitation, these are the main arguments in support of this scenario. There are also a number of counterarguments to these estimates, similarly well grounded and of about the same weight.

The global oil and gas industry hardly goes forward through the problems caused by the fall in oil prices which began in the summer of 2014. Following restructuring, reduction of activity, cuts in expenditures and cancelled investment projects, the professionals in the oil and gas sector believe that the industry’s recovery, meaning the oil prices and the resumption of investments, will start in 2017 or at the latest in 2018 – but a lot of them believe that the process has already begun!

Oil prices – estimates

The worse seems to have passed for the global industry of oil and gas, as the ‘2016 Oil & Gas Industry Survey: Optimism Emerges In The Aftermath Of A Long Downturn’ paper reads, published by the consulting company Deloitte in mid September 2016; The survey – conducted in June and July based on interviews with a sample of 251 professionals (of all levels and all sectors – from upstream to services) – shows that 86% have an optimistic outlook on the industry, saying it has already entered a recovery phase, or will reach that phase no later than in the next two years. More specifically, 33% of respondents expect a start of the industry’s recovery in 2017, 24% believe that this phase has already begun, and 28% of those surveyed believe that it will begin no later than 2018 (see the graph ‘Next two years will bring rising prices and investments for the oil and gas industry’). In this positive scenario, e.g. 61% of them believe that the WTI oil could reach USD 60 per barrel by the end of 2016 at the latest, and another 44% believe the price will evolve in the range of USD 60-80 per barrel in 2017 at the latest (see the graph ‘Expectations for the WTI oil price’); the estimates regarding Brent oil price developments closely follow the ones for WTI.

‘The feeling’ coming from the Deloitte survey is interesting in several respects, but particularly in that it confirms the estimates of some professionals with the large financial institutions – like the World Bank or Bank of America Merrill Lynch.

At the end of July, World Bank experts modified the average oil price forecast for 2016 from USD 41 to USD 43 per barrel. “We expect a slight increase in oil prices in H2, on the background of pressure easing generated so far by overproduction,” reads the press release sent to the public by John Baffes, economist with the World Bank and author of this report; the positive outlook on oil prices – encouraging element for the industry, was confirmed by the projections for the next decade, published by the same report (see the table ‘World Bank estimates’), revealing an upward trend.

World Bank estimates

Also at the end of July, the Bank of America Merrill Lynch (BofA) analysts released a report pointing also to a positive outlook on the oil and gas industry, arguing that only a recession or a great shock on the supply side would have the power to bring oil prices back below USD 40 per barrel; their estimates were of USD 46 and USD 45 per barrel (Brent and namely WTI) as average for 2016. “The influences coming from cyclical factors have become less significant against the seasonal ones in recent years. We see the oil prices declining in Q3 this year. Prepare for a W-shaped recovery. The uncertainties in Nigeria and Venezuela could influence the oil price in both ways,” American analysts say in the report, predicting a return to levels of USD 55 and namely USD 54 per barrel at the end of 2016, after reaching a minimum of USD 39 per barrel in September (see the table ‘Bank of America Merrill Lynch estimates’).

As benchmark, in late September the price of WTI oil was on an obvious downward trend (confirming the BofA analysts expectations on the W shaped developments), being traded at around USD 45 per barrel – i.e. still above the lows estimated by them (see the graph ‘The oil price development in the last decade of September’).

As benchmark, in late September the price of WTI oil was on an obvious downward trend (confirming the BofA analysts expectations on the W shaped developments), being traded at around USD 45 per barrel – i.e. still above the lows estimated by them (see the graph ‘The oil price development in the last decade of September’).

Pros

The industry-wide feeling revealed by the Deloitte survey therefore appears to be an extension of the forecasts made by the economists of the above mentioned institutions… the difference being that the latter’s outlook is based on a series of arguments, calculations and assumptions clearly mentioned in the reports. And if we look at the most recent one – the BofA report – we notice that the American analysts reasoning is based on the existence of premises indicating an imminent change in the ratio between oil demand and supply (ratio currently characterized by oversupply).

Thus, according to BofA analysts, the global investment cuts over the last approximately 18 months – from about USD 690 billion in 2014 to about USD 410 billion in 2016 – has already begun to register the first negative effects; the signal is given by the pace of introduction into service of new deposits that is no longer counterbalancing the depleting speed of deposits in operation – the reserves declining rate is growing worldwide. The phenomenon of growing depletion rate of the oil deposits is noticeable in particular in non-OPEC countries, where the natural decline rate has grown from 4.87% in 2009 to 5% (at a rate even higher than expected by BofA economists, who estimated only 4.9% this year). However, this phenomenon is also noticeable in some OPEC countries – Venezuela, Algeria and Angola are among the OPEC members that can record decreasing output due to the cuts in investment programmes, BofA estimates reveal. The trend of accelerated pace of depletion is thus a first prerequisite. In parallel, world economy continues the positive development, driving oil demand to an upward trend; with a significant contribution coming from Asia, where China in particular, but also other economies in the region, fully benefit from the very favourable context of low interest rates from the major central banks of the world. The low level of interest stimulates the so-called ‘chasing yields’ which direct the investments towards the emerging economies, whereas cheap money stimulates consumption, generating additional demand for oil.

The two overlapping trends (non-OPEC oil supply cut and increasing consumption) would lead to the gap increase between supply and demand, BofA analysts said – a difference which, being difficult to cover by the OPEC members, will put pressure on the price increases.

Falling production

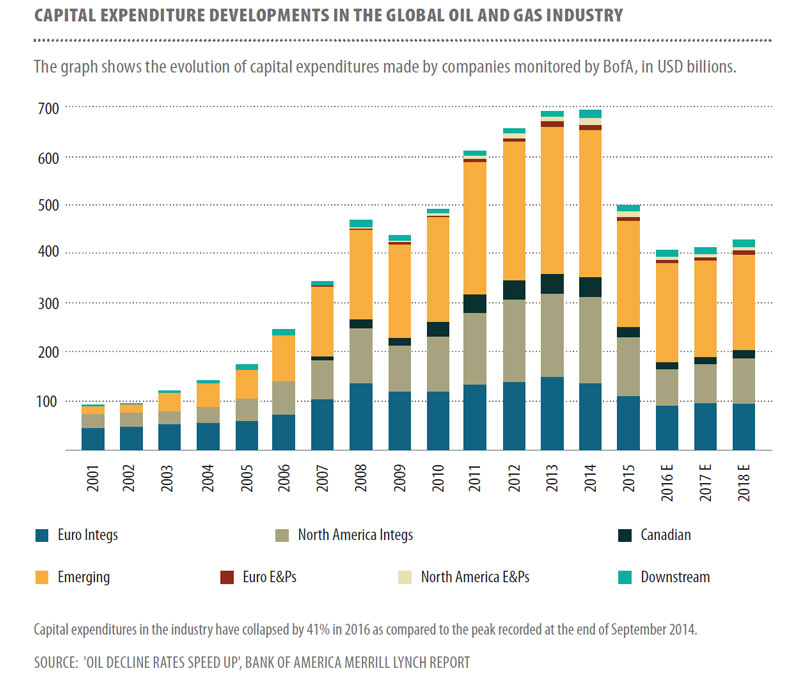

“Decisions to cut investments are having their say now,” BofA analysts say! The global oil and gas industry capital expenditures at the end of July 2016 were by about 41% lower (namely the equivalent of about USD 280 billion) as compared to the peak in 2014; all regions recorded decreases in this index (see the graph ‘Capital expenditure developments in the global oil and gas industry’); North America led by far in this race.

In the United States the outcome of these decisions has resulted in the sharp decline in the number of the wells drilled, which fell from a peak of 1,931 in September 2014 to only 447 at the end of July 2016 and in the oil production, which fell from 9.7 million barrels per day (mb/d) in April 2015 to 8.9 mb/d in April 2016. This trend is now beginning to be visible also for other oil producers – at the beginning for non-OPEC countries, even if the process is barely in its first phase – BofA analysts reveal. They believe the effect of capital expenditure cuts are transmitted to the production levels, similarly to the way price movements do (price movements spread into production within about 12 months; on the other hand, in contrast to production from unconventional deposits – which respond to price adjustments in about 9 to 18 months – the conventional projects have a slightly larger response time). Based on these premises, BofA analysts claim that the decrease in capital expenditures for oil production begins to be felt as of the second year of the process – which means that most of the effects of the disinvestment cycle started in 2015 will start occurring in 2017 and could last until 2021.

The BofA economists’ outlook is not at all unique: in December 2015 the Norwegian company Rystad Energy – one of the most renowned consultants in the oil industry opined that a possible new production crisis in the oil market “is only a few years away”, based exactly on the same reasoning. Patrick Pouyanne – CEO of French company Total, based on estimates for projects in the upstream sector and on the need for new production capacities needed on the market to offset the natural decline of deposits – warned of the risk that by 2020 the oil market could reach a supply deficit of up to 10 million barrels per day.

The decrease of capital expenditures leads to the speeding of operational deposits depletion, but not all regions of the world answer to that impulse, BofA analysts explained, arguing that the decline has a higher speed in non-OPEC countries in the Middle East and in the OECD Member States in the Pacific region (see the graph ‘Natural decline rate of deposits under exploitation, up in non-OPEC countries’). Thus, the non-OPEC countries in the Middle East recorded, in late July 2016, a deposits’ depletion rate (according to BofA estimations/calculations) of about 18% and in OECD countries in Asia and Africa the rate was of approximately 12%.

BofA analysts expect the deposits’ rate of decline in non-OPEC countries to grow further, which will lead to lower output. In a natural move, major producers such as Saudi Arabia and other producers in the GCC (Gulf Cooperation Council – a regional political and economic organization made up by states of the Persian Gulf, comprising Bahrain, Kuwait, Oman, Qatar, Saudi Arabia and the United Arab Emirates) to which would add Iraq and Iran, might try to cover this potential breach; moreover, most of the extra production/supply share on the market in recent years comes precisely from Saudi Arabia, Iraq and Iran.

The problem lies in the fact that these countries have a more limited capacity to respond to new challenges, BofA analysts say. The number of wells drilled in Iraq has dropped to about half during the last 24 months; Iran is already close to the maximum level of production possible, and Saudi Arabia has not succeeded in bringing into operation any project to offset the decrease by 37% in the number of wells recorded at the end of July 2016 against the peak in 2014. This happens while the risks and tensions in the region make the prospects of investments in the Persian Gulf remain rather modest. “On these considerations we argue that the global oil demand will increase by 0.2 million barrels/day in 2017 – whereas the demand for oil will grow by 1.2 million barrels per day, which would represent a driving force for oil price increases up to an average level of USD 61 per barrel for 2017 as a whole,” BofA analysts conclude in the report.

The BofA experts’ position is complemented by data from the International Energy Agency revealing that Iran and Iraq, as well as Kuwait, United Arab Emirates and Venezuela, were at the end of August 2016 close to their maximum production capacity.

Demand and supply

The BofA estimates on oil demand growth are in line with those made by the Energy Information Administration (EIA – US specialized agency) claiming in the ‘Global Petroleum and Other Liquid Fuels’ report published in early September, that globally the consumption of oil and other liquid fuels will increase in 2016 by 1.5 mb/d and by other 1.4 mb/d in 2017; the largest part of this additional demand will come from non-OECD countries (these countries have recorded an additional demand of 0.9 mb/d in 2015, and their consumption will increase by 1.2 mb/d in 2016 and by other 1.3 mb/d in 2017); India and China are the main contributors to this dynamic, the domestic consumption of the two countries is estimated by EIA on an upward trend by 0.3 and respectively 0.4 mb/d in 2016 and 2017.

On the other hand, the trends of cutting output by non-OPEC countries and of higher global demand (items used by the Bank of America as basic premises in their forecasts) are also prospective developments for the Organization of Oil Producing Countries (OPEC) ‘Monthly Oil Market Report’ released on September 12, 2016. Thus, the report said the global oil demand will increase by 1.23 mb/d in 2016 up to the level of 94.27 mb/d and by other 1.15 mb/d in 2017 to 95.42 mb/d – mainly due to the extra demand coming from India and China – as expected also by EIA (see the graph ‘Estimates for oil demand during 2016-2017’). In parallel, as BofA analysts anticipate, the OPEC experts too say the oil production of non-OPEC states will go down in 2016 (by 0.61 mb/d to 56.32 mb/d), but will slightly increase in 2017 (by 0.2 mb/d to 56.52 mb/d) (see the graph ‘Estimates for oil demand during 2016-2017’). They argue that the demand for OPEC oil will be in 2016 of about 31.7 mb/d (by about 1.7 mb/d more than in 2015), and will reach 32.5 mb/d in 2017 (by 0.8 mb/d above the level estimated for 2016) (see the graph ‘OPEC and non-OPEC estimates for 2016 and 2017’).

It is obvious that the actual impact of the increasing rate of oil deposits decline – when we talk about an output of 95 million barrels per day, it is difficult to calculate because each deposit has its own characteristics, being operated under different technologies. In the report ‘World Energy Outlook’ in 2013, however, the EIA estimated that average natural decline rate is of about 2% per year for conventional fields, with the prospect of rising to 4% in late 2020s. This projection was made when the oil price was USD 100 per barrel and was expected to remain at that level until 2020; now, in a world where the oil price is estimated to reach, at best, USD 50 to USD 70 per barrel over the next years, the rate of decline could easily double. This means that only due to this phenomenon, out of the oil output/supply could vanish in 2016 and 2017 between 1.4 and 3.6 million barrels (of daily production volume).

A player with high potential

If the increase in demand and falling output are elements supporting the scenario for the oil and gas industry’s revival – Iran’s entry on the market and lower output costs are two of the counter-arguments against this scenario. Thus, in the first scenario, analysts believe that the emergence of a shortage in supply would be crucial for prices increases – not few are those who argue that the entry of Iran on the market after lifting the sanctions is likely not only to counterbalance such an upward trend, but to put additional pressure on their decline.

Iran is indeed a potentially major player. The problem lies in the fact that it is already close to the maximum output that it can achieve. In late May 2016, Iran reported an output of 3.5 million barrels per day and aimed to reach the level of 4.8 mb/d by 2021. Nevertheless, just for achieving this objective, investments of about USD 70 billion are needed, an amount which, in the current context, is difficult to obtain: China has its own domestic problems (to cope with), and Europe is still reluctant to invest in Iran. The relationship with Europe is anyway already difficult enough if we consider that Italy – once one of the best customers for Iranian oil, has waited more than five months after the lifting of sanctions for the first sea transport, whereas Spain and Greece have levels of trade (imports) still far below the one before sanctions. Under these circumstances, the US Agency EIA experts believe that Iran can at the most reach a production of 4.1 mb/d – assuming that it will succeed to attract capital and technology and it will not get back to sanctions – actually not insignificant, they argue.

Cons

The ‘Iran’ counterargument, although powerful and leading to effects so far (Iran’s entering the market is one of the determinant factors for accelerating the downward trend of oil prices!), it seems therefore the most compelling element to counterbalance the BofA analysts scenario (which argue that the deepening gap between supply and demand could be determinant for increasing oil prices).

In contrast, however, the ability of unconventional deposits oil producers to reactivate quickly under favourable price conditions represents a counterargument to consider! It is thus clear that the phenomenon of closing down the wells, consequent to falling prices, can be run in reverse in the case of price increases. Every dollar up in oil prices makes the alternative oil exploitation more cost effective, in other words it increases the likelihood they are resumed. Therefore, the US alternative oil fields producers become ‘swing producers’ (i.e. those players who have the ability to influence trends) for the market. Particularly that innovation and the development of operating technologies continuously put pressure on the operating costs, leading them down!

The part played by the production cost in the equation, resulting in production levels, is yet significantly more complex! The cost of producing a barrel of oil – which is on a downward trend – can be a factor to stop the possible exaggerated momentum of oil price on international markets; on the other hand, however, in this equation an important role is played by the cost of money! Let’s not forget that the ‘explosion’ of alternative oil deposits was caused and supported by the injections of money on financial markets and by the Fed’s interests policy, more or less close to zero! The Fed made money to be not only very cheap but also abundant, stimulating investments of any type (as risky as they may have been) and thus, in particular, in the investment in the exploitation of oil and gas unconventional deposits.

However, today, in a context where the Fed is getting closer to the time of the first interest increase (estimated by analysts to take place at the last monetary policy sitting this year – in December), it is obvious that this ‘driving force’ (of cheap and plentiful money!) cannot operate on the same parameters. Higher funding costs for such projects and lower amounts of money available on the market for projects with a high degree of risk (as the exploiting of alternative deposits) will be increasingly more difficult in terms of reactivation and as development of new alternative exploitations.

And yet

Arguments brought forward by the analysts who support the imminent revival of the oil and gas industry (i.e. return of oil prices and investment) are therefore offset by the serious arguments of those who claim that higher output obtained due to technological advances and to the declining costs may temper the oil demand growth trend. Nevertheless, they have, in turn, as seen above, many questions marks in terms of consistency and reality.

Fundamentally, however, it is clear that independent of all elements that may influence demand and/or supply (cost of production, technological advances, development of technology for renewable sources, etc.) there is a limit to the speed with which technologies using fossil fuels are being replaced. On the other hand, billions of people in the third world increase the consumption per capita every day, this trend is significantly stronger and faster than in the developed world that relies on renewable energies and on energy efficiency to respond to climate changes. This means that the trend of increasing the net energy consumption is likely to continue for at least a generation from now – considering the emerging economies’ pace and the pattern of development. In this scenario, the prospect of higher oil prices and the recovery of the oil and gas industry become as realistic as possible!