Accenture Study: 30% of Europe’s Largest Listed Companies Have Pledged to Reach Net-Zero by 2050

Corporate commitments to net-zero accelerated over the last two years, with almost one-third (30%) of Europe’s largest listed companies now having pledged to reach net-zero by 2050, according to a new study by Accenture.

The Accenture study, ‘Reaching Net Zero by 2050,’ analysed data from more than 1,000 listed companies across Europe’s major stock indexes, finding that setting targets helps accelerate the transition to net-zero — i.e., where a company reduces its emissions of CO2 and other greenhouse gases (GHG) to zero or offsets the remainder to achieve a balance between the amount of GHG emissions produced and the amount removed from the atmosphere. Last decade, the companies with a net-zero goal reduced their emissions by 10% on average, while those without targets saw their emissions increase.

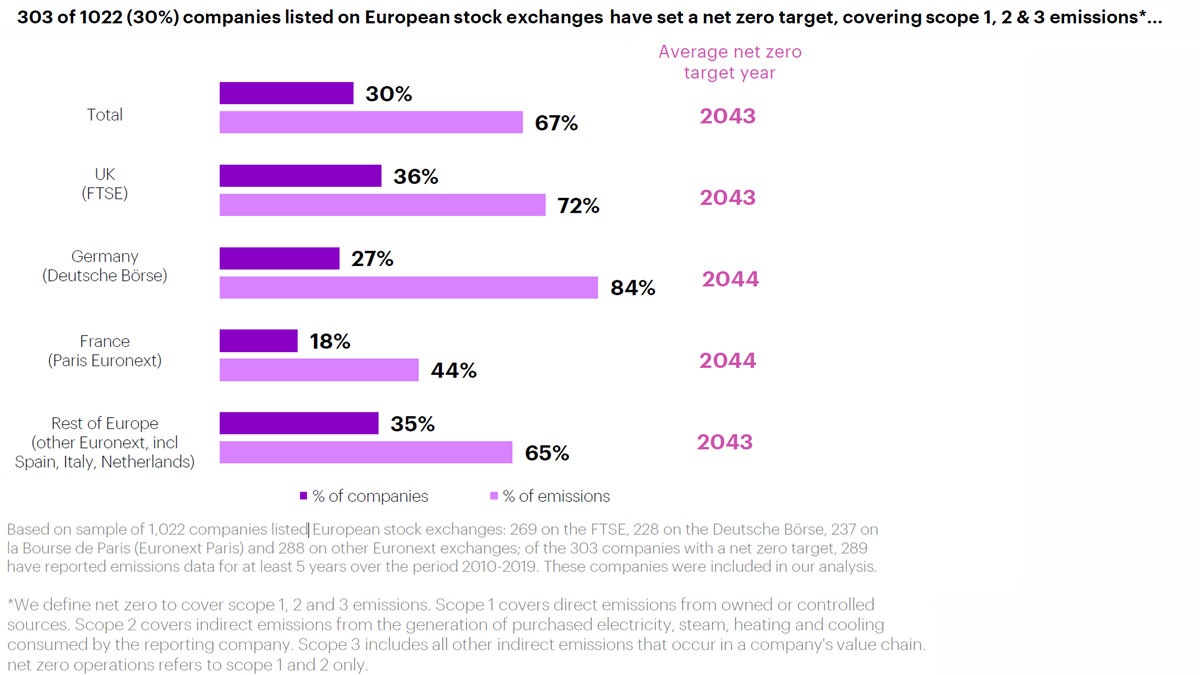

Companies listed in the U.K. were the most likely to have set a net-zero target date, covering scope 1, 2 and 3 emissions*, with 37% having done so, compared with 27% in Germany and 18% in France.

The average net-zero target year for European companies included in the study is 2043. Many companies in carbon-intensive industries — such as oil and gas and chemicals — have set net-zero target dates of or close to 2050, while many in services sectors aim for around 2035.

“The European business community is more engaged than ever in the race to zero, with the number of companies publicly setting goals having grown over the last two years,” said Jean-Marc Ollagnier, CEO of Accenture in Europe. “And as our study shows, the targets work. Net zero should be managed as any strategic business priority: set clear objectives to drive the entire organization to the same direction and monitor progress to correct the trajectory as appropriate. Making targets public also helps create the required collective momentum, as companies can’t solve it alone.”

Accelerated action needed as just 5% of companies on track to meet their targets

However, the study found that just one in 20 (5%) of the European companies in the study are on track to achieve their net-zero target dates in their own operations, covering scope 1 and 2 emissions, if they continue the pace of emissions reduction that they achieved between 2010 and 2019, with only 9% on course to meet a 2050 target. Companies that have achieved modest emissions reduction since 2010 — i.e., 0-5% reduction per year —can still reach net-zero in their operations before mid-century if they double the pace of emissions reduction by 2030 and triple it by 2040.

“Though the number of newly set targets is reassuring, it is still clear that organizations are not moving fast enough,” said Peter Lacy Accenture’s chief responsibility officer and Sustainability Services global lead. “With COP26 just a few weeks away, businesses and governments across all parts of the world need to focus their efforts on concrete action that follows robust targets to meet the challenge our world faces to reach net zero by mid-century and hold global warming to 1.5°c.”

The report suggests specific solutions and stepping-stones to net zero for select industries, including automotive, chemicals, construction, finance, retail, and transportation.

It also shows that seven industries — mostly in service sectors such as professional services and information and communications — will be on track for net-zero in their operations by 2050 if they double the pace of emissions reduction in this decade, and then accelerate another 50% to 70% in the following 10 years. More radical acceleration will be needed for five sectors representing 42% of GHG emitted by all companies in the research sample — automotive, construction, manufacturing, oil & gas, and transportation & storage — to reach net-zero by mid-century.

“Net-zero by 2050 — let alone sooner — will be feasible only with swift, decisive action in this decade. Our findings show that it is possible, but only if European businesses act now,” Ollagnier said. “Solutions differ by industry and company, and all have different starting points, opportunities and challenges. In some industries, the required technologies are available and will need to be scaled at speed. In others, they will have to be invented. However, getting there will require all businesses to make reinvention the norm, driven by technological innovation, collaboration, new business models and supportive regulation.”

Most companies will need to take more radical action

56% of companies that have achieved modest emissions reductions since 2010 can achieve net zero operations before 2050 if they double the pace of emissions reductions by 2030 and triple it by 2040; others will need to do even more.

On sector-specific emissions reduction pathways, based on consensus expert knowledge about the best available technology for reducing emissions, 25% of companies in this sample would meet their own net zero target year and more than half would reach net zero operations before 2050.

Even with accelerated action—doubling the pace of emissions reduction by 2030 and then doubling it again by 2040—just 42% of companies in this sample would reach net zero operations in line with their own targets, and 83% before 2050.

Doubling the pace of emissions reduction in a decade would put seven industries on track for net zero operations by 2050

However, on sector-specific emissions reduction pathways, five sectors, representing 42% of emissions, still would not reach net zero in their own operations by mid-century.

Joint action on value chain emissions can get everyone all to the right side of 2050

The growing commitment of European businesses to address emissions in their value chain (scope 3) will be a critical step to get more companies and industries to reach net zero before 2050.

Greater and faster strides in reducing emissions can be made when working together, along value chains and across industries. For example, collaboration between steel producers and petrochemical companies in scaling green hydrogen production for low-carbon steel manufacturing will help automotive companies accelerate the pace of emissions reduction. And the investment of the automotive sector in increasing the availability and affordability of electric vehicles will help fleet electrification and decarbonisation in the transport sector and beyond.

About the Research

The research is based on data collected by Retail Economics about the net-zero targets (covering scope 1, 2 and 3 emissions) of 1,022 of Europe’s largest listed companies: 269 on the FTSE, 237 on Euronext Paris, 228 on the Deutsche Börse, and 288 on other Euronext exchanges, including 73 Italian companies and 54 Spanish companies. Researchers analysed the emissions from 2010 to 2019 of companies in the report sample, focusing on the absolute scope 1 & 2 emissions (excluding scope 3 to avoid double counting), and the compound annual reduction rate (CARR) of emissions over the 10-year interval was calculated.

Projections of potential emissions reduction pathways for each company in the dataset were built to estimate in which future five-year time interval the company is likely to reach net zero. An ‘S-curve’ shape was chosen for the projections, in line with existing expert scenarios for emissions reduction by industry. Company-level projections to industry and country level were aggregated to assess the period over which companies in the industry and country are likely to achieve net zero. Finally, the net-zero target years were compared with the time interval resulting from the emissions pathway analysis.

* Scope 1 emissions are GHG direct emissions from companies’ own and controlled resources. Scope 2 covers indirect emissions from the generation of purchased energy — i.e., purchased electricity, steam, heating and cooling consumed by the reporting company. Scope 3 includes all other indirect emissions that occur in a company’s value chain.