Decarbonisation: The Challenges of the Great Transition

Since the 70s, the world has experienced soaring growth in its energy demands, mainly fed by fossil fuels and centralized power generation. The future, however, should and seems to be expected as different. Transformations of any kind do not appear from a vacuum; especially when we speak about energy transformation and even more specifically in such a crucial sector like that of Energy.

Transformation is shaped by a much broader and fundamental shift in terms of prosperity, progress, politics, and the environment. We see signs of that shift even in the terminology, shifting from ‘green’ to ‘smart and sustainable’. We call this wider and fundamental shift in context ‘The Great Transition’. One of the cornerstones of this huge transition is ‘decarbonisation’. This ongoing transformation does not only concern and apply the energy sector, or a switch from one fuel source to another, or merely the technological leap. It is much broader and reflects a shift, a transformation, in terms of values and also the way we understand the world around us nowadays.

As mentioned, we observe a gradual breakaway from the older core values of security, reliability, and robustness which existing energy systems were built on, to new values of sustainability, flexibility, and affordability, enabled by a completely new way of producing, delivering, and consuming energy. This does not necessarily mean that the older frame of values will become obsolete or irrelevant anytime soon, but the centre of weight is definitely being rebalanced.

The notion

The notion of decarbonisation translates in a few words as the reduction of carbon inputs to socioeconomic metabolism or of greenhouse gas (GHG) emissions such as CO2 or CH4. Indicators such as GHG emissions per unit of technical energy, are widely used in climate-related discourses.

They are often expressed as kilogram CO2 equivalent per year. Different GHGs are converted into CO2 equivalents according to their respective global warming potentials. Partial decarbonisation can be achieved by increasing the share of low-GHG fuels such as hydropower or solar in total energy supply. In theory, it is possible to reduce net carbon emissions to zero or even achieve net negative emissions if technologies such as bioenergy with carbon capture and sequestration are used on a large scale.

However, on the input side, socioeconomic metabolism cannot be entirely decarbonised because biomass is indispensable for socioeconomic metabolism, at least as food and feed, and the carbon content of dry matter biomass amounts to 45–50%. Therefore, we are facing a dual challenge: that of the emissions coming from the energy sector but also other sectors like agriculture (dairy, meat etc.)

The process

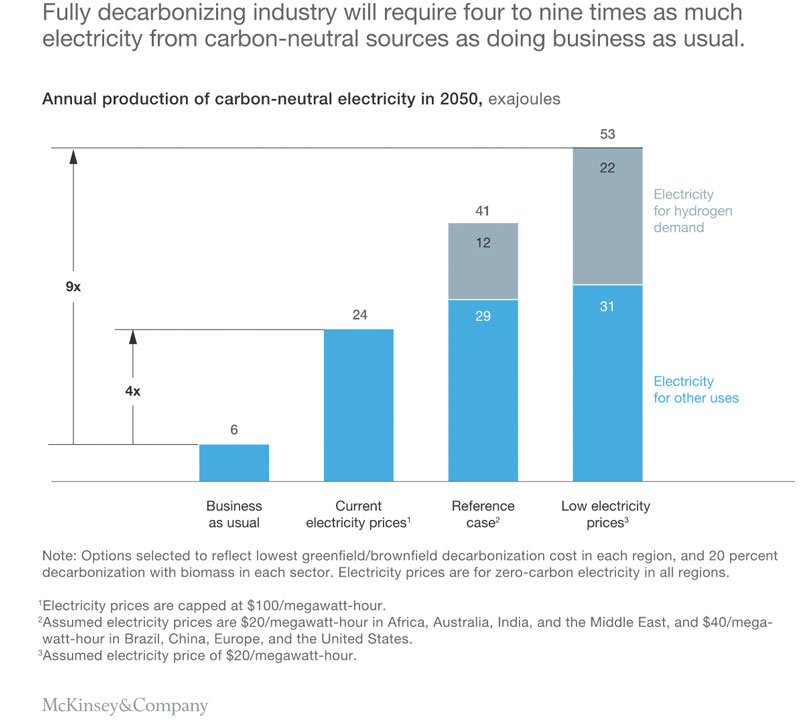

Lowering industrial GHG emissions is a very realistic task, but not an easy one. A report coming from the leader in the Consulting world, McKinsey, is revealing. The report called ‘Decarbonization of industrial sectors: The next frontier’, finds that elements like ammonia, cement, ethylene, and steel companies can reduce their carbon-dioxide (CO2) emissions to almost zero with energy-efficiency improvements, the electric production of heat, the use of hydrogen and biomass as feedstock or fuel, and carbon capture.

Discussion about transitions and transformation is never easy and the financial aspect always frames the discussion; cash is King Afterall. The decarbonisation of the above-mentioned sectors would cost between USD 11 trillion and USD 21 trillion all the way until 2050 and will require accelerating the extension and deployment of renewable-energy capabilities, to provide four to nine times as much clean power as industry would need in the absence of any effort to reduce emissions.

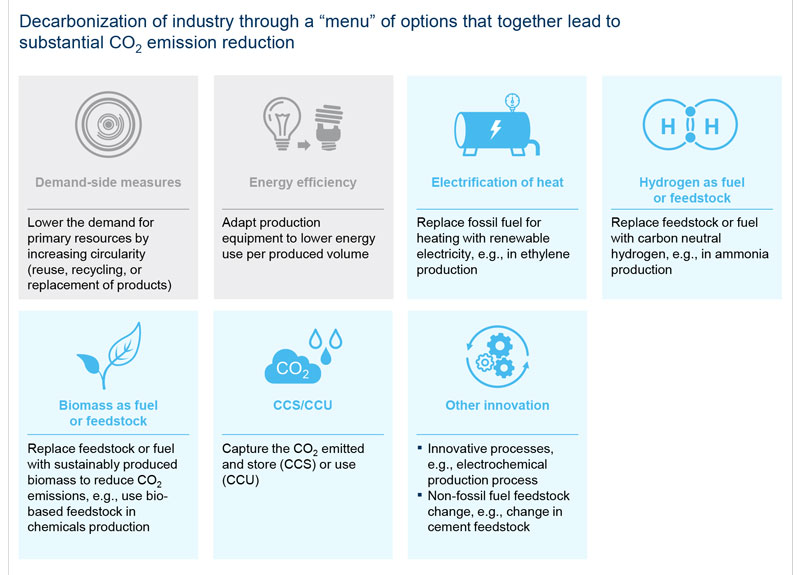

Despite the challenges described above, companies in the four focus sectors could bring their CO2 emissions close to zero with a combination of approaches. The most promising are:

- Energy-efficiency improvements;

- The electrification of heat;

- The use of hydrogen made with zero-carbon electricity as a feedstock or fuel;

- The use of biomass as a feedstock or fuel;

- And carbon capture and storage (CCS) or usage (CCU).

The optimum mix of decarbonisation options would be apparently variable and different combinations could be used to address the needs and potential specificities. The same principle could apply even within the same sector, because local factors determine which ones are most practical or economical. Decision makers must evaluate their options on a site-specific basis by closely examining these factors.

The most important factors are the availability and cost of low-carbon energy sources—specifically, zero-carbon renewable electricity and sustainably produced biomass. Access to storage capacity for captured CO2, along with public and regulatory support for carbon storage, will affect the possibility of implementing CCS. The regional-growth outlook for the four focus sectors matters, too, because certain decarbonisation options are cost effective for existing (brownfield) industrial facilities while others are more economical for newly built (greenfield) facilities.

Industrial companies must prepare for decarbonisation by conducting a detailed review of all their capacities, resources, facilities and by looking at the availability of low-cost electricity, hydrogen, biomass, and carbon-storage capacity. This process should have a primary goal of hitting maximum efficiency. Achieving the dual transformation of the energy and industrial sectors will require coordinated efforts across the economy. Other key players and stakeholders should be brought into the mix for finding opportunities for collaboration: co-investing in a shared carbon-storage infrastructure, for example, or supporting research and development for promising decarbonisation technologies. The public sector would be a great example, due to its nature and of course, bringing its regulatory capacity into the game.

Governments can develop road maps for industrial decarbonisation on the local and regional levels to create a more certain outlook for industrial and power companies and unlock investments with flexible and longer payback times. Governments can also adjust regulations and incentives to support decarbonisation—for example, encouraging investment in renewable-generation capacity by altering the financial requirements on utilities and other companies involved in generating and distributing energy. Energy leaders from around the world including national and regional policymakers have a critical role to play in driving forward the development of a coordinated Action Plan to better realize opportunities for aligning decarbonisation of energy supply with existing infrastructure that may need to be appropriately dealt with. In Europe, besides national governments, European policymakers will have a key role for energy infrastructure plan to ensure coherence for all the countries.

All in all, industrial companies can drastically lower their carbon emissions, but only by collaborating with other stakeholders and the public sector. Joint planning and timely action can accelerate the development of low-carbon technologies for industry and help to coordinate the dual transformation of the energy and industrial sectors. For industrial companies and other organizations, the time to begin the transition is now.

Decarbonisation: Going Deeper

One of the apparent conclusions, deeply connected with the notion of maximum efficiency, is that there can be no waste of resources. This clearly indicates the direction of reusing or repurposing the already existing infrastructure. The transition will heavily depend on infrastructure that is adaptable, reliable and affordable. Going further, we need to consider that the existing energy infrastructure has been built around conventional resources over many decades with trillions of dollars in investment. It will be a missed opportunity to not plan for the role of existing infrastructure in future energy systems.

The need is clear and the opportunities lies ahead: use of existing infrastructure is a resource for more affordable transition to decarbonisation. According to leaders and key decision makers within the energy sector, all around the world, it is concluded that one of the obstacles to a successful energy transition is exactly the efficient repurposing of the existing resources. Furthermore, a factor would be that of asset decommissioning and the stranded assets. What is more alarming, is that despite its significance, existing infrastructure has become an undiscussable challenge and is insufficiently planned for: dealing with existing infrastructure is an afterthought to decarbonising the supply of energy. Arguably, it can be said with a fair amount of certainty that:

- An integral part of the opportunity is the consideration of infrastructure repurposing opportunities where these make sense;

- The extent to which assets are stranded. This is currently a variable and unknown factor which presents us with a potential risk of decarbonisation becoming cost-prohibitive if large portions of existing infrastructure are stranded.

Decarbonisation: ‘The Great Transition’ Projects

Dealing effectively with existing infrastructure, whilst not inevitable, is not impossible. We have excellent cases of joint integral project showcasing how the Great Transition should and could be performed.

NextStep: A joint initiative of EBN and the Dutch oil and gas industry, is the only holistic action plan developed in the world to date to deal with existing infrastructure. The National Platform for Re-use & Decommission and the Dutch oil and gas industry, represented by NOGEPA act with the clear ambition to contribute to the safe and environmentally friendly re-use and decommissioning of oil and gas infrastructure in Holland.

NexStep plans to stimulate and facilitate the Dutch agenda for re-use and decommissioning of oil and gas infrastructure with the aim to:

- Have zero safety incidents;

- Create minimum environmental impact;

- Realize cost reductions through efficiency.

Due to the foreseen, and not only, decline of hydrocarbon production in the future, the oil and gas infrastructure should be repurposed for other uses. The energy transition presents a tremendous opportunity to re-use existing elements to complement renewable investments before the eventual safe and efficient decommissioning. As the great champion and the face of re-use and decommissioning of oil and gas infrastructure in the Netherlands, the joint venture aims to engage stakeholders and the general public about their work. They plan based on a dedicated innovative agenda which will identify new challenges and promote technology development where it is needed. NexStep will also encourage industry collaboration, and exactly the cooperation formula that we talked about earlier, sharing of lessons learned and engagement with international partner organizations involved in the coordination of re-use and decommissioning of oil and gas infrastructure.

California’s Action Plan: Although not directly dealing with infrastructure, offers an effective model of how to bring an industry together under a common vision. In their ‘Roadmap to Decarbonize California’s Buildings’ today, a coalition of key players and stakeholders from the public and private sector lays out a plan for the state to cut building emissions by more than 20% within the next decade and by 40% by 2030. Another aligned goal is to adopt zero-emission building codes for residential and commercial buildings by 2025 and 2027, respectively. “Reducing the environmental impact of homes and buildings is both an environmental imperative and an economic opportunity,” said Lauren Faber O’Connor, chief sustainability officer for the City of Los Angeles. “This roadmap shows that together, we can cut energy consumption and reduce costs at the same time—showing the world that going green is good for your health and bottom line.”

The Roadmap, developed by a coalition of public sector and private stakeholders, addresses a range of market and policy barriers preventing mass adoption of zero-emission appliances.

“As the electricity sector becomes cleaner, we need a range of tools and programs providing customers more choices for cleaner, safer electric technologies, including heat pump water and space heaters,” said Jill Anderson, vice president customer programs and services, Southern California Edison. “The Building Decarbonization Coalition’s Roadmap is a visionary vehicle addressing one part of the overall economy-wide set of actions needed to meet California’s ambitious climate goals while maintaining affordability for customers.”

The Roadmap also lays out a plan to ensure an equitable approach and support vulnerable communities already struggling against skyrocketing housing costs and stagnating wages are protected as California moves toward zero-emission technologies. To achieve this, the Roadmap calls for low-cost, easily accessible financing options, re-aligning existing programs to help communities achieve carbon-free homes and implementing measures such as bulk purchasing, subsidizing installations and contractor training.

DDPP: A global collaboration of energy research teams charting practical pathways to deeply reducing greenhouse gas emissions in their own countries. They are indeed on a huge task and aiming to achieve what is needed to limit global warming to 2°C or less.

The DDPP is a collaborative initiative to understand by showcasing how countries can transition to a low-carbon economy by mid-century and how the globe can reach the internationally agreed target of limiting the increase in global mean surface temperature to well below 2 degrees Celsius (°C). The project also organizes low-carbon technology roundtables to contribute to the mobilization of a global public and private Research, Development, Demonstration and Diffusion (RDD&D) effort to drive directed technical change.

The DDPP framework has been developed and utilized by a consortium led by The Institute for Sustainable Development and International Relations (IDDRI) and the Sustainable Development Solutions Network (SDSN). It currently consists of scientific research teams from leading research institutions in sixteen of the world’s largest greenhouse gas emitting countries. More specifically, the 16 Country Research Teams composed of leading researchers and research institutions are from countries representing over 70% of global GHG emissions and different stages of development: Australia, Brazil, Canada, China, France, Germany, India, Indonesia, Italy, Japan, Mexico, Russia, South Africa, South Korea, the UK, and the USA.

The DDPP will support interested countries in developing mid-century “low greenhouse gas emission development strategies mindful for 2°C and 1.5°C” as called for in the Paris Agreement on climate change.

The Scenarios for the Future

Approximately a century ago, in April 1896, Svante Arrhenius published an article, ‘On the Influence of Carbonic Acid in the Air upon the Temperature of the Ground’. It was actually the first comprehensive study to analyse the ‘greenhouse effect’ and to assess the harmful impact of elevated concentrations of CO2 (carbonic acid in the terminology of Arrhenius) in the environment.

He quantified the CO2 emissions quoting estimates of his colleague, Professor Hogborn, indicating consumption of some half a billion tons of coal worldwide (and assessed them to equal the carbon uptake by weathering of rocks). The greenhouse effect and the potential of anthropogenic interference of CO2 emissions from burning of fossil fuels have been actually known and studied by science for 100 years.

The study presented the calculations parametrically for a range of CO2 concentration levels from 200 to 900 ppmv (parts per million by volume), compared to the then estimated prevailing level of about 300 ppmv. And 100 years later, CO2 concentrations have reached 360 ppmv and numerous scenarios exist that attempt to project emission levels far out into the future.

The most significant finding for these scenarios is that after the middle of the 21st century carbon intensities stay constant for all of the six scenarios developed. This represents in our viewpoint a certain lack in scenario richness, especially in view of the stated purpose to explore a wide range of future possible developments through the scenario exercise. There, only one scenario portrays a similar picture of stagnating improvements in decarbonization as depicted by the IPCC scenarios. The IS92 scenario assumptions of driving forces in the domain of energy technologies and resource availability appear restricted, especially when compared with the wide variation in input assumptions like population and economic growth.

Decarbonisation: ‘The Great Transition’

The global energy system is indeed gradually decarbonizing, as measured by the reduction in the specific carbon emissions per unit of primary energy consumed. This trend appears continuous and persistent.

Should these historical trends continue, we might in fact be only half-way through the fossil fuel age that would draw to a close only late in the 22nd century. The driving forces of decarbonisation include both continued technological change in all domains of energy production, conversion, and end use as well as the quest for higher flexibility, convenience, and cleanliness of energy services demanded by consumers, especially as incomes rise.

To an extent the energy sector ‘compensates’ some of the more pronounced decarbonisation trends in energy end use, reflecting resource endowments, technology availability, geopolitical considerations, as well as policy influence. This gives reason to be cautiously optimistic that development and the resulting economic growth, increased energy needs, and emissions could be reconciled with a precautionary policy of avoiding large-scale human interference with the climate system.

The task of controlling energy-related carbon emissions, as daunting as it may appear from today’s perspective, may in fact turn out to be less obstructive if indeed an acceleration of long-term structural change trends is called for rather than departure in an entirely new direction. Conversely, it will simply not suffice to rely on ‘autonomous’ structural change toward carbon-freer energy systems, especially considering the slow historical rates of decarbonisation of 0.30Jo per year. They are dwarfed by historical an anticipated future growth rates in energy use and resulting carbon emissions. Substantial acceleration of decarbonisation would thus entail both ambitious technological and policy changes. Whereas such changes are inherently difficult to anticipate, it is also a matter of fact that historically it was precisely structural changes that enabled us to improve quality and quantity of energy services. Such structural changes are rarely represented in studies of energy-environment interactions. This suggests that decarbonisation and its driving forces may still be insufficiently captured in most models and scenarios of the long-term evolution of the energy system.

Any Great Transition is always subject to uncertainty, obscurity but also hope for ‘tomorrow’; there is currently a continuous torrent of initiatives, formulating into a river of change. This is exactly the type of change that our species needs, even if it is not the mainstream attitude for the time being. As always, a few will lead the way and we must remember: “Those crazy enough to think they can change the world, are the ones they do”.