Gas for Climate – A path to 2050

The optimal role for gas in a net-zero emissions energy system

A study recently published, performed by Navigant for the Gas for Climate consortium, serves as a follow-up to their study published in 2018, including a greatly expanded scope and analysis.

While achieving 100% greenhouse gas reduction requires large quantities of renewable electricity, by far the most cost optimal role to decarbonise is by combining electricity with renewable gases such as hydrogen and biomethane. Renewable gas adds value in the heating of buildings, for high temperature industrial heat, providing flexibility in electricity production alongside wind and solar and in heavy transport.

Using around 2900TWh or approximately 270 billion cubic meters of renewable methane and hydrogen in a smart combination with renewable electricity saves society EUR 217 billion across the energy system compared to reducing gas to an absolute minimum. Existing gas infrastructure is indispensable in transporting this renewable and low carbon gas to the various demand sectors. Gas infrastructure can be used to transport both hydrogen and biomethane in 2050.

The Navigant experts foresee an initial important role for blue hydrogen (carbon-neutral hydrogen produced from natural gas with carbon capture and storage), to grow the developing hydrogen market including in new applications. Towards 2050, with increased levels of renewable electricity and falling costs, renewable green hydrogen will gradually replace blue hydrogen, achieving in the end a fully renewable energy system.

“The new Gas for Climate study shows that gas and its infrastructure will play an indispensable role in the future decarbonised energy system together with electricity infrastructures. We support the transition to a fully renewable energy system in which biomethane and green hydrogen will play a major role in a smart combination with renewable electricity while recognising that blue hydrogen can accelerate decarbonisation efforts in the coming decades,” the CEOs of the nine Gas for Climate members said in a joint statement.

The purpose of this study is to assess the cost-optimal way to fully decarbonise the EU energy system by 2050 and to explore the role and value of renewable and low-carbon gas used in existing gas infrastructure. This is being done by comparing a ‘minimal gas’ scenario with an ‘optimised gas’ scenario. The study is an updated version of the February 2018 Gas for Climate study, with an extended scope of analysis.

The current study adds an analysis of EU energy demand in the industry and transport sectors. It also includes an updated supply and cost analysis for biomethane and green hydrogen, including dedicated renewable electricity production to produce hydrogen, and an analysis on power to methane. Finally, it assessed the potential role of blue hydrogen, natural gas combined with carbon capture and storage (CCS) or carbon capture and utilisation (CCU).

Both the ‘minimal gas’ and ‘optimised gas’ scenarios arrive at a net-zero emissions EU energy system by 2050. The scenarios both assume a significant increase in renewable electricity (wind, solar PV, and some hydropower). The main difference between the scenarios is the role of renewable and low carbon (or ‘decarbonised’) gas, and the role of biomass power. The ‘minimal gas’ scenario decarbonises the EU energy system assuming a large role for direct electricity use in the buildings, industry and transport sectors, with some biomethane being used to produce high temperature industrial heat. Renewable electricity is produced from wind, solar and hydropower, combined with solid biomass power. The ‘optimised gas’ scenario also has a strongly increased role of direct electricity in the buildings, industry and transport sectors. Yet it concludes that renewable and low-carbon gas will be used to provide flexible electricity production, to provide heat to buildings in times of peak demand, to produce high temperature industrial heat and feedstock, and to fuel heavy road transport and international shipping.

Study’s main conclusions

- Full decarbonisation of the energy system requires substantial quantities of renewable electricity in both study scenarios. Electricity production will more than double and renewable electricity production from wind and solar-PV will increase ten-fold compared to today.

- Strong growth in wind and solar PV requires dispatchable electricity production by either solid biomass or gas. Battery seasonal storage is unrealistic even at strongly reduced costs.

- Full decarbonisation of high temperature industrial heat requires gas in both scenarios.

- Existing gas grids ensure the reliability and flexibility of the energy system. They can be used to transport and distribute renewable methane and hydrogen.

- It is possible to sustainably scale-up renewable gas–biomethane, power to methane and green hydrogen–at strongly reduced production costs.

- Blue hydrogen produced from natural gas combined with CCS can be a scalable and cost-effective option. Because green hydrogen is still expensive today and because its ramp-up is linked to the speed of growing wind and solar capacity to necessary levels, an early scale-up of blue hydrogen can accelerate decarbonisation.

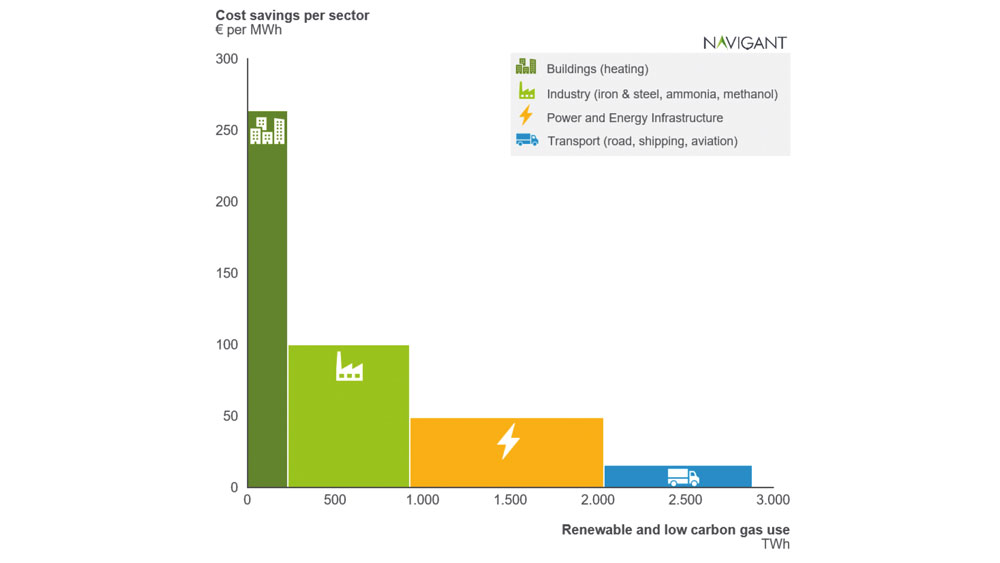

- The ‘optimised gas’ scenario allocates 1,170TWh renewable methane and 1,710TWh hydrogen to the buildings, industry, transport, and power sectors. This equals about 270 billion cubic metres of natural gas (energy content). Compared to the ‘minimal gas’ scenario, the use of gas through gas infrastructure saves society EUR 217 billion annually across the energy system by 2050.

- The ‘minimal gas’ scenario requires 809TWh of (probably partly imported) solid biomass power, nine times more than the 89TWh in ‘optimised gas’.

- The future energy system can become fully renewable, with blue hydrogen being replaced by renewable green hydrogen towards 2050–2060 following a large scale-up of wind and solar.

These conclusions are in line with the results of the 2018 Gas for Climate study. Especially conclusions 1-3, the biomethane scale-up potential mentioned under conclusion 5, the large energy system cost savings under point 7 and the large role for solid biomass power under point 9 are similar to what was concluded in the previous study. The current study shows larger gas volumes (2900TWh versus 1000TWh) and energy system cost savings (EUR 217bn versus EUR 138bn annually) following a more extensive analysis into hydrogen supply and into energy demand in industry and transport.

As shown in the graph below, cost savings per unit of energy are highest in the heating of buildings, where renewable gas is used combined with electricity in hybrid heat pumps in buildings that are connected to gas grids today. Also, the use of renewable gas in electricity production generates significant energy system savings because it avoids costly investments in solid biomass power or even costlier battery seasonal storage. Using less solid biopower in ‘minimal gas’ would increase the costs of this scenario and therefore increase the cost savings by implementing ‘optimised gas’.

The total annual costs amount to more than two trillion euro in both scenarios. Most of these costs are not additional costs related to decarbonisation but are regular energy system costs and transport vehicle costs that exist today as well. For all relevant uses of energy, Navigant chose the scope of the cost estimates that enabled it to perform a fair cost comparison between the two scenarios. This means that the study included all energy production costs for both scenarios, yet for road transport it includes road vehicle and fuel costs, while for aviation it only includes fuel costs because the costs for aeroplanes will be similar in both scenarios. Also, cost for upgrades in the electricity transmission grid are fully included, while low voltage distribution is not because strong electrification in both scenarios would result in similar grid replacement costs. It can safely be concluded that the EUR 217 billion euros cost savings in the ‘optimised gas’ scenario are a substantial share of additional costs beyond ‘business as usual’ energy system costs.

In addition to substantial reductions in additional energy system costs, the ‘optimised gas’ scenario has non-cost related benefits including promoting rural employment from increased biomethane production and avoiding unnecessary new overhead powerlines that could meet societal opposition.

Although reduced compared to today, the EU will still require large quantities of energy in 2050. In our 2050 scenarios domestic sources of coal and nuclear are (almost) phased out, raising the question where required energy will be produced. Today, the EU imports more than 50% of its energy. In theory it is feasible to produce all required energy in both study scenarios domestically within the EU by 2050. However, producing renewable energy in other parts of the world can be an attractive alternative, and it is more likely that international trade in energy will continue to exist. This could include imports of solid biomass in the ‘minimal gas’ scenario or imports of green hydrogen in the ‘optimised gas’ scenario.

The ‘optimised gas’ scenario includes only renewable gas to show that it is possible to achieve net-zero emissions by 2050, with no remaining role for low-carbon gas. Yet because the costs of green and blue hydrogen can be similar by 2050, there could still be a role for blue hydrogen. Blue hydrogen can grow the use of low-carbon hydrogen in coming years, allowing faster decarbonisation. Towards 2050, natural gas will be phased out and blue hydrogen would increasingly be replaced by green hydrogen and renewable methane. The speed by which green hydrogen can replace blue hydrogen depends on how fast all direct electricity demand can be produced from renewables and how fast additional renewable electricity generation capacity is constructed beyond that. It furthermore depends on whether policy makers will limit the use of blue hydrogen by 2050. Any large scale-up of green hydrogen production prior to the moment when all demand for direct electricity is covered by renewable power results in indirect increases in fossil electricity generation.

This study analyses the optimal 2050 decarbonised energy system; it does not include detailed analysis on the way to get there. In developing the system towards the desired 2050 state, it can be effective to transport blended methane and hydrogen through gas grids in coming years with hydrogen shares of up to 10% in transported gas, while gradually creating dedicated hydrogen transport grids by retrofitting part of the existing gas grids. Likewise, while by 2050 biomethane adds more value in buildings and electricity production and light transport can be expected to be electrified, it can make sense to continue to use bio-CNG in transport today to create an initial market for sustainable biomethane, and to accelerate transport decarbonisation.

Further details on key study conclusions

- Large increase in renewable electricity

Full decarbonisation of the EU energy system in a cost-optimal way requires substantial quantities of renewable electricity in both study scenarios.

- Renewable methane and hydrogen provide cost-effective dispatchable power

Either solid biomass, large-scale battery seasonal storage or renewable or low-carbon gas is required to provide dispatchable electricity production once wind power and solar PV are scaled more than tenfold by 2050. Renewable methane and hydrogen supplied through gas infrastructure provide dispatchable electricity and offer seasonable storage in a cost-effective way.

- Biomethane and power to methane

Biomethane and power to methane can supply up to 1,170TWh at strongly reduced costs, consisting of 1,010TWh of biomethane and 160TWh of power to methane.

Navigant’s analysis shows that by 2050 all biomethane can be zero emissions renewable gas, in the sense that any remaining lifecycle emissions can be compensated by negative emissions created in agriculture on farms producing biomethane. Based on the assessment of potential biomethane cost reductions the study concludes that production costs can decrease from the current EUR 70–90/MWh to EUR 47–57/MWh in 2050. These costs reflect large-scale biomass to biomethane gasification close to existing gas grids, as well as more local biomethane production in digesters.

An assessment of the feasibility of increasing renewable methane production by methanation of CO2 captured in biogas upgrading showed that this technology could increase the renewable methane potential although costs will remain somewhat higher than biomethane or hydrogen costs.

Navigant’s assessment on the biomethane potential has not significantly changed from its 2018 analysis, now 95bcm instead of the previous 98bcm of natural gas equivalent. In response to questions and comments on the uncertainties of the supply of sustainable silage when implementing Biogasdoneright (winter silage cropping) throughout Europe the potential in southern Europe versus countries with a more moderate climate is now differentiated. Navigant performed a deeper analysis of the availability of woody biomass for biomethane, including short-rotation plantation wood cultivated on abandoned farmland.

- Green hydrogen

Dedicated wind and solar PV generation could produce green hydrogen as the main product.

Navigant found that there is large theoretical potential of offshore wind and solar PV, going beyond the estimated 2050 EU renewable power projection. This means that the technical potential for green hydrogen production is virtually limitless. However, there are considerations such as the land use change risks associated with an increase in non-rooftop solar PV and competing sea uses to offshore wind that will limit the green hydrogen potential. The costs of hydrogen based on dedicated renewable electricity can come down to about EUR 52/MWh.

Navigant found that pipeline transport of green hydrogen is the most economical and that shipping hydrogen will likely remain expensive due to high costs of liquefaction. While imports of hydrogen to the EU are possible, the most likely option would be hydrogen produced in neighbouring regions (e.g. North Africa) being transported to Europe through pipelines. Mixing hydrogen with methane is possible but is unlikely to be the optimal solution by 2050.

- Blue hydrogen as a valuable temporary energy carrier

Navigant concludes that the technical potential for blue hydrogen based on using permanent carbon capture and utilisation (CCU) in the EU is small. However, blue hydrogen based on applying CCS can be scaled up to very large quantities within a relatively short timeframe to 1,500TWh, or 142bcm natural gas equivalent. However, limited political acceptance today is a barrier to scaling up CCS. To increase political acceptance, policymakers can ensure that blue hydrogen plays a role as a bridge fuel to achieve net-zero emissions faster compared to a fully renewable system. To ensure that blue hydrogen will be a net-zero emissions gas in 2050, the remaining 5–10% of uncaptured CO2 needs to be compensated elsewhere in the energy system by then. This can be done by using biomethane in combination with CCS. In 2050, the estimated cost of blue hydrogen is comparable to green hydrogen. This means that pro-active policy to ensure the greening of hydrogen supply is required.

- 2050 demand for electricity and gas in both study scenarios

The ‘minimal gas’ and ‘optimised gas’ scenarios both require a large increase in renewable electricity. Also, full decarbonisation of high temperature industrial heat requires a share of renewable gas in both study scenarios. Yet significant differences between both scenarios exist. In the ‘optimised gas’ scenario, existing gas infrastructure is used to transport and distribute 1,170TWh renewable methane and 1,710TWh hydrogen to the EU buildings, industry, transport, and power sectors. This corresponds to a 2050 gas consumption of 272 billion cubic metres of natural gas equivalent (in terms of energy). The ‘minimal gas’ scenario assumes that gas infrastructure would be mostly decommissioned and flexibility in the electricity system will be either provided by expensive solid biomass power or even more expensive battery seasonal storage. Battery storage remains expensive compared to gas grid storage, even if battery costs reduce to EUR 60,000 per MWh of storage capacity by 2050. It should be noted that renewable methane use is supply-driven whereas hydrogen use is demand driven. Furthermore, hydropower and liquid biofuel are supply-driven and direct electricity consumption throughout the energy system is demand driven.

- Electricity production and heating of buildings

Navigant analysed the possible role of hydrogen and biomethane in electricity production and heating of buildings based on the updated supply potentials. The outcomes differ little from the previous study. In both ‘optimised gas’ and ‘minimal gas’ scenario most buildings will by 2050 be heated by all-electric heat pumps, and both scenarios assume increased levels of district heating. In the power sector, now also hydrogen is used for dispatchable electricity generation.

For heating of buildings, in the ‘optimised gas’ scenario all buildings with gas connections today will continue to use gas by 2050, mainly biomethane and some hydrogen used during periods of peak demand in hybrid heat pumps, in combination with electricity.

Gas consumption per building will be much lower by 2050 compared to today. The ‘minimal gas’ scenario assumes that only all-electric heat pumps and district heating will be available.

- Industry

Navigant assessed the expected 2050 energy demand in the iron and steel, ammonia and methanol, and cement and lime industries, as well as the optimal net-zero emissions energy mix. The assessment concluded that industrial low temperature heat will be mostly based on direct electricity in both study scenarios. High temperature industrial heat is mainly provided by hydrogen in both scenarios, plus some biomethane and hydrogen as industrial feedstock. CCS will be needed to reduce process emissions, for example, from steelmaking and cement production. The difference between both scenarios is that in ‘minimal gas’ green hydrogen is produced at industrial sites, not requiring gas infrastructure, whereas in ‘optimal gas’ green hydrogen is produced close to large-scale (offshore) electricity generation and transported to demand hubs using existing gas infrastructure.

- Transport

Navigant also assessed scenarios to fully decarbonise EU transport by 2050 and the potential role for renewable and low-carbon gas, focusing on road transport (passenger cars, trucks, and buses), shipping, and aviation. Shipping and aviation include domestic and intra-EU shipping and aviation, as well as intercontinental fuelling and bunkering. We conclude that EU transport energy demand can be reduced by half in both study scenarios from today’s 4500TWh to about 2100TWh by 2050. Light road transport (passenger cars, light commercial vehicles) and domestic shipping will be primarily electric in 2050 in both study scenarios. Long-distance heavy transport requires fuels with a high energy density, meaning that direct use of electricity (from batteries) is less suitable for international shipping and aviation. In heavy road transport and international shipping, hydrogen and bio-LNG dominate in the ‘optimised gas’ scenario while large quantities of biodiesel are used in the ‘minimal gas’ scenario. Aviation will continue to use kerosene, being a mix of bio jet fuel and synthetic kerosene in both scenarios.

While multiple parallel fuelling options are implemented locally, the energy mix for long-haul truck transport, shipping, and aviation must be internationally uniform. It is not feasible for one country to fuel ships with liquified biomethane (bio-LNG) while a neighbouring country offers biodiesel. In aviation, the two most promising renewable fuels, bio jet fuel and synthetic kerosene, can use the same fuelling infrastructure as today.

Maintaining gas infrastructure generates EUR 217 billion in annual energy system cost savings

The European gas transmission and distribution (T&D) network consists of approximately 260,000 km of high-pressure network of which 200,000 km are operated (mainly) by transmission system operators (TSOs), plus approximately 1.4 million km of medium and low-pressure pipelines operated by distribution system operators (DSOs). Gas infrastructure ensures the reliability and flexibility of the energy system. Navigant expects gas transmission and distribution networks to still have a valuable role by 2050, transporting biomethane and hydrogen. In both scenarios described in this study, volumes of gas used in networks are lower in 2050 than in 2019. Still, the use of gas in existing infrastructure will generate significant net energy system cost benefits.

Compared to the ‘minimal gas’ scenario, the use of this gas through existing gas infrastructure saves society EUR 217 billion annually across the energy system. Cost savings per unit of energy are highest in the heating of buildings, where renewable gas is used combined with electricity by means of hybrid heat pumps, in buildings that are connected to gas grids today. Also, the use of renewable gas in electricity production generates significant energy system savings because it avoids costly investments in solid biomass power or even costlier battery seasonal storage.